Once property taxes are one-year delinquent on a property, the county government is going to hold a sale and offer tax lien certificates for sale on all of the delinquent properties. As investors, we can attend these sales and acquire tax lien certificates that pay you 8% to 36% interest per year depending on which county we’re investing in. Again, you don’t have to go to auctions to acquire tax lien certificates; it’s simply the way the process begins.

When you acquire a tax lien certificate, by law, you are now the first position lien holder of record. In essence what you did was pay the delinquent tax bill, and in return you received a Tax Lien Certificate. When the delinquent property taxes are paid, you receive all of your original investment back, plus the secured high interest rate.

Each state has a redemption period, or grace period in which the delinquent property taxes must be paid. Redemption periods range from 6 months to 3 years depending on which county you’re investing in.

Each state has a redemption period, or grace period in which the delinquent property taxes must be paid. Redemption periods range from 6 months to 3 years depending on which county you’re investing in.

If the delinquent property taxes are not paid within the redemption period, the lien holder may exercise his or her right to initiate the judicial process of property tax foreclosure. Once this process is complete, the tax lien certificate investor will receive the deed to the property free and clear with no mortgage.

Property tax law clearly states that once this process is complete, "tax foreclosure will result in the loss of ownership of the property and all rights of all interested parties…" which gives you a free and clear deed to the property.

When informed investors conduct proper due diligence, and acquire tax lien certificates on the right types of properties, there are only two outcomes: 1) the tax lien certificate redeems, and the investor receives all of their money back plus the state-mandated rate of interest (8-36%), or 2) the tax lien certificate does not redeem, and the investor receives a free and clear deed to the property with no mortgage for literally pennies on the dollar.

A Tax Lien Certificate is a first position lien on real estate due to delinquent property taxes. Once property taxes on a property are one year delinquent, the county government is going to offer a tax lien certificate on the property. Tax lien certificates pay fixed rates of returns of 8% to 36% interest per year depending on which county you’re investing in. The price of the tax lien certificate is the amount of one years back taxes and penalties, and therefore can range in price from under $100, to hundreds of thousands of dollars.

A Tax Lien Certificate is a first position lien on real estate due to delinquent property taxes. Once property taxes on a property are one year delinquent, the county government is going to offer a tax lien certificate on the property. Tax lien certificates pay fixed rates of returns of 8% to 36% interest per year depending on which county you’re investing in. The price of the tax lien certificate is the amount of one years back taxes and penalties, and therefore can range in price from under $100, to hundreds of thousands of dollars.

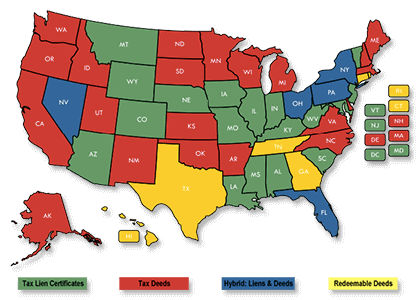

No. About half the states in the United States offer Tax Lien Certificates, and the other half offer Tax Deeds. Both systems offer very lucrative investment opportunities for the informed investor. Both are means of collecting delinquent property taxes, putting properties back on the tax roll, and generating revenue to the county for schools, police departments, roads, hospitals, fire departments, and libraries.

No. About half the states in the United States offer Tax Lien Certificates, and the other half offer Tax Deeds. Both systems offer very lucrative investment opportunities for the informed investor. Both are means of collecting delinquent property taxes, putting properties back on the tax roll, and generating revenue to the county for schools, police departments, roads, hospitals, fire departments, and libraries.

Each state has a redemption period, or grace period in which the delinquent property taxes must be paid. Redemption periods range from 6 months to 3 years depending on which county you’re investing in.

Each state has a redemption period, or grace period in which the delinquent property taxes must be paid. Redemption periods range from 6 months to 3 years depending on which county you’re investing in.

Some counties will identify these types of challenged properties on their lists. Other counties will remove these challenged properties from their list completely. We always advise our students to complete thorough due diligence no matter what. After 27 years of real world, in the field experience, we’ve learned the most accurate information we can rely on is from our own due diligence.

Some counties will identify these types of challenged properties on their lists. Other counties will remove these challenged properties from their list completely. We always advise our students to complete thorough due diligence no matter what. After 27 years of real world, in the field experience, we’ve learned the most accurate information we can rely on is from our own due diligence.

No! When you and I acquire a tax lien certificate, in essence what we’re doing is paying someone else’s delinquent property tax bill for them. In return, we receive a tax lien certificate on the property, which bears the interest rate. Because the tax lien certificate has a grace period

of 6 months to 3 years, we just bought the property owner time. Rather than taking advantage of someone in financial trouble, we did just the opposite; we gave them the opportunity to stay in their home for an additional 6 months to 3 years.

No! When you and I acquire a tax lien certificate, in essence what we’re doing is paying someone else’s delinquent property tax bill for them. In return, we receive a tax lien certificate on the property, which bears the interest rate. Because the tax lien certificate has a grace period

of 6 months to 3 years, we just bought the property owner time. Rather than taking advantage of someone in financial trouble, we did just the opposite; we gave them the opportunity to stay in their home for an additional 6 months to 3 years.

Most people don’t lose their primary residence for a couple of hundred, or couple of thousand dollars in back taxes. The vast majority of tax lien certificates on primary residences do redeem, which insures fixed, high rates (8-36%) of interest to the investor.. The typical single-family residential home that doesn’t redeem is usually some sort of rental property, many times with an out of state or absentee owner. Thousands and thousands of these types of properties get

acquired through the tax lien certificate process every year.

Most people don’t lose their primary residence for a couple of hundred, or couple of thousand dollars in back taxes. The vast majority of tax lien certificates on primary residences do redeem, which insures fixed, high rates (8-36%) of interest to the investor.. The typical single-family residential home that doesn’t redeem is usually some sort of rental property, many times with an out of state or absentee owner. Thousands and thousands of these types of properties get

acquired through the tax lien certificate process every year.

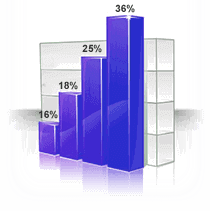

Many of our successful clients have no interest in owning real estate, and feel much more comfortable just earning high interest only. You can definitely invest in tax lien certificates and earn the high interest rates of say 18%, or 25%, or 36% interest, and basically eliminate the possibility of owning the property.

Many of our successful clients have no interest in owning real estate, and feel much more comfortable just earning high interest only. You can definitely invest in tax lien certificates and earn the high interest rates of say 18%, or 25%, or 36% interest, and basically eliminate the possibility of owning the property.

If you’re interested in acquiring real estate, then you’re going to want to invest in "Tax Deed" states, and also use the "Tax Resale Property" acquisition strategy.

If you’re interested in acquiring real estate, then you’re going to want to invest in "Tax Deed" states, and also use the "Tax Resale Property" acquisition strategy.

There are three basic types of tax lien certificate sales: premium bidding, rotation bidding, and bid down the interest rate.

There are three basic types of tax lien certificate sales: premium bidding, rotation bidding, and bid down the interest rate.

Investing in tax lien certificates isn’t complicated. It’s a matter of understanding the rules and procedures for the markets you have an interest in, and then knowing how to complete thorough due-diligence in a timely manner. Once you understand the due-diligence process, you can successfully acquire tax lien certificates anywhere in America – right from the comfort of your own home – in as little as four hours a week, or even less. Like most anything else, the more time and effort you dedicate, the more successful you can become.

Investing in tax lien certificates isn’t complicated. It’s a matter of understanding the rules and procedures for the markets you have an interest in, and then knowing how to complete thorough due-diligence in a timely manner. Once you understand the due-diligence process, you can successfully acquire tax lien certificates anywhere in America – right from the comfort of your own home – in as little as four hours a week, or even less. Like most anything else, the more time and effort you dedicate, the more successful you can become.

A tax lien certificate is a non-commissionable investment vehicle, i.e. counties do not pay commissions on Tax Lien Certificates. Stockbrokers, financial planners, and banks can recommend tax lien certificates, but they wouldn’t make a commission if they did. Tax lien certificates that pay you 18% or 25% interest per year would compete greatly with their "safe" investment vehicles that do pay commissions, but only pay the investor 1% or 2% interest per year.

A tax lien certificate is a non-commissionable investment vehicle, i.e. counties do not pay commissions on Tax Lien Certificates. Stockbrokers, financial planners, and banks can recommend tax lien certificates, but they wouldn’t make a commission if they did. Tax lien certificates that pay you 18% or 25% interest per year would compete greatly with their "safe" investment vehicles that do pay commissions, but only pay the investor 1% or 2% interest per year.

The interest rate, redemption period (grace period), and collection procedures are set and enforced by state law. Each state has its own set of rules, regulations, and procedures.

The interest rate, redemption period (grace period), and collection procedures are set and enforced by state law. Each state has its own set of rules, regulations, and procedures.